Jumbo Loan: Exactly How to Receive Larger Home Financing

Jumbo Loan: Exactly How to Receive Larger Home Financing

Blog Article

Discovering the Advantages and Qualities of Jumbo Loans for Your Next Home Purchase Choice

As the actual estate market develops, understanding the ins and outs of big lendings ends up being significantly pertinent for potential homebuyers considering high-value buildings. To completely appreciate just how jumbo financings can affect your home purchase technique, it is necessary to explore their vital features and benefits in greater detail.

What Is a Jumbo Finance?

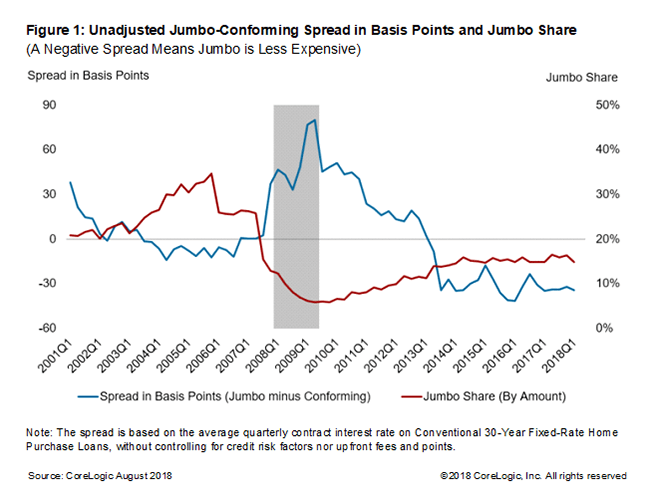

Jumbo finances are often made use of by purchasers looking for to purchase high-value properties or homes in pricey markets. jumbo loan. Provided the bigger quantities borrowed, lenders typically impose stricter credit rating requirements, consisting of greater credit report, lower debt-to-income ratios, and bigger deposits. The rate of interest rates on big lendings might be somewhat greater than those on adhering lendings, mirroring the boosted risk for lending institutions

Additionally, the approval process for a big funding can be more intricate and lengthy, as loan providers call for substantial documentation to examine the borrower's economic stability. Comprehending these subtleties is crucial for potential property owners taking into consideration a jumbo financing for their residential property financing requirements.

Secret Advantages of Jumbo Loans

One substantial benefit of jumbo finances is their capacity to fund higher-priced properties that surpass adapting financing limits. This feature makes them an appealing alternative for customers looking to buy deluxe homes or residential or commercial properties in high-cost areas where rates generally exceed standard funding thresholds.

Additionally, jumbo car loans commonly feature versatile terms and affordable interest rates, enabling debtors to tailor their financing to suit their unique economic situations. jumbo loan. This versatility can consist of choices for adjustable-rate home loans (ARMs) or fixed-rate finances, offering purchasers with the capability to manage their monthly payments according to their choices

An additional advantage is that big car loans do not need private mortgage insurance (PMI), which can considerably decrease the overall price of the loan. With PMI typically being a substantial expense for standard fundings with reduced deposits, preventing it can cause considerable financial savings gradually.

Furthermore, customers of jumbo financings usually have accessibility to greater car loan amounts, allowing them to spend in residential or commercial properties that fulfill their way of life needs. This gain access to equips customers to act decisively in affordable realty markets, protecting their desired homes better. Overall, big financings provide essential benefits for those seeking to fund premium properties.

Eligibility Needs for Jumbo Lendings

Jumbo finances come with particular eligibility demands that possible borrowers need to meet to safeguard financing for high-value homes. Unlike standard car loans, which have established restrictions based on the conforming financing limits established by government-sponsored entities, big lendings exceed these thresholds, requiring more stringent criteria.

Furthermore, jumbo lendings often demand a significant down settlement, typically varying from 10% to 20% of the purchase rate, depending on the loan provider's policies and the borrower's monetary circumstance. Meeting these qualification demands can position customers positively in securing a jumbo finance for additional resources their wanted home.

Comparing Jumbo Loans to Standard Financings

Recognizing the differences in between big car loans and traditional car loans is necessary for buyers browsing the high-end realty market. Jumbo car loans surpass the conforming financing restrictions established by the Federal Real Estate Finance Company (FHFA), which implies they are not qualified for acquisition by Fannie Mae or Freddie Mac. This causes different underwriting requirements and demands for customers.

On the other hand, conventional car loans typically comply with these limits, allowing for an extra streamlined authorization procedure. Big fundings often need stricter credit report ratings, bigger down payments, and greater financial books. For instance, while a standard funding may call for a down settlement of as little as 3% to 5%, jumbo loans usually demand a minimum of 10% to 20%.

Interest rates on jumbo loans may vary from those of standard fundings, often being a little greater due to the enhanced risk lenders think - jumbo loan. However, the possibility for substantial financing can be useful for customers seeking high-end properties. Eventually, understanding these differences enables property buyers to make enlightened choices, aligning their funding options with their distinct purchasing needs and monetary scenarios

Tips for Protecting a Jumbo Car Loan

Protecting a big lending requires cautious planning and preparation, as loan providers commonly enforce stricter requirements compared to standard loans. To boost your possibilities of authorization, begin by inspecting your credit history and attending to any kind of issues. A rating of 700 or greater is generally preferred, as it shows credit reliability.

Following, gather your economic documentation, consisting of tax obligation returns, W-2s, and financial institution statements. Lenders generally need site link comprehensive proof of income and possessions to analyze your capability to repay the finance. Keeping a low debt-to-income (DTI) ratio is likewise essential; objective for a DTI below 43% to boost your application's competition.

Additionally, take into consideration making a bigger deposit. Several loan providers look for a minimum of 20% down for big fundings, which not only decreases your loan amount but also signals monetary stability. Engaging with a knowledgeable mortgage broker can provide vital understandings right into the process and aid you browse different lending institution options.

Final Thought

In summary, big fundings existing substantial advantages for property buyers looking for residential properties that surpass standard lending restrictions. With affordable rate of interest, versatile terms, and the absence of private home loan insurance, these loans can cause considerable cost financial savings. Potential consumers need to navigate more stringent eligibility requirements to get favorable terms. Extensive understanding of both the benefits and needs connected with big fundings is essential for making informed home acquisition choices in an affordable property market.

The passion prices on jumbo lendings may be a little higher than those on adhering loans, mirroring the boosted threat for lending institutions.

While a standard car loan could call for a down repayment of as little as 3% to 5%, jumbo finances normally necessitate a minimum of 10% to 20%.

Rate of interest prices on jumbo loans may differ from those of traditional financings, typically being somewhat greater due to the increased threat lenders read this article assume.Protecting a big finance needs careful planning and prep work, as lenders usually enforce stricter demands compared to standard lendings. Numerous lending institutions seek at the very least 20% down for big loans, which not only reduces your car loan amount however likewise signals economic stability.

Report this page